What the One Big Beautiful Bill Act Means for Student Loan Borrowers

On July 4, 2025, the One Big Beautiful Bill Act—a sweeping legislative package—was signed into law, bringing with it some of the most significant changes to federal student loans in over a decade.

If you’re a borrower, a parent, a recent graduate, or even a future student considering college, these changes could affect how much you can borrow, how you repay, and how long you’ll stay in debt. The policy shifts are complex, but you don’t have to face them alone. Let’s walk through what’s changing, what it means for you, and what steps you can take now.

Goodbye to Unlimited Borrowing

For years, Parent PLUS and Grad PLUS loans allowed families and graduate students to borrow up to the full cost of attendance. That’s changing.

Under the new law:

Parent PLUS Loans are now capped at $20,000 per year per student and $65,000 lifetime.

Note: These loans will no longer be eligible for income-driven repayment plans after July 1, 2026.

Grad PLUS Loans will be eliminated entirely for new borrowers beginning July 1, 2026.

– Graduate students can still borrow through Direct Unsubsidized Loans, with new limits:

– General advanced degrees: $20,500/year, $100,000 lifetime (previously $138,500)

Undergraduate loan limits remain unchanged.

The total federal loan cap per borrower is now $257,500, which includes both undergraduate and graduate borrowing.

What This Means: If you’re pursuing an expensive graduate or professional program, you may need to seek additional funding—or reconsider the financial viability of certain schools.

Simplified Repayment Options

Federal loan repayment is being streamlined. Beginning July 1, 2026, borrowers will have only two repayment options:

1. Standard Plan

This is a fixed monthly payment plan based on your total loan balance:

Under $25,000 – 10-year term

$25,000 to $49,999 – 15-year term

$50,000 to $99,999 – 20-year term

$100,000 or more – 25-year term

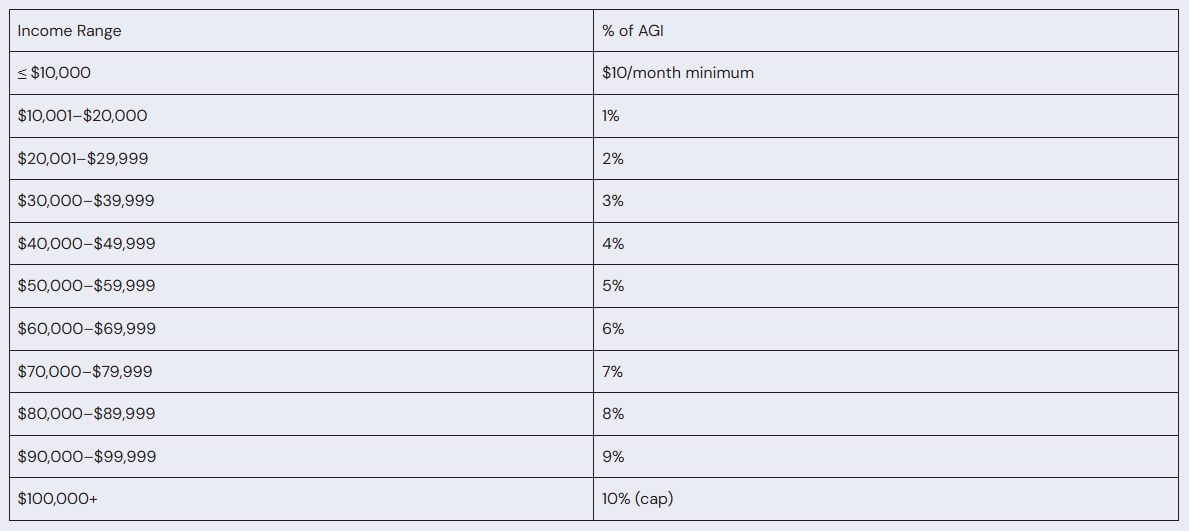

2. Repayment Assistance Plan (RAP)

This new income-driven plan ties payments to your income, ranging from 1% to 10% of your Adjusted Gross Income (AGI):

Additional RAP Features:

$50/month deduction per dependent. This means your calculated monthly payment would be reduced by $50 for every dependent you have.

Monthly principal reduction: If your payment doesn’t reduce your principal by $50, the government will cover the difference to ensure your principal balances decrease. For example, if your monthly payment only makes a dent of $40 to the principal, then the government will pitch in another $10. Borrowers whose monthly payments already reduce their principal balance by at least $50 would get no extra help from the government.

Interest forgiveness: If your required monthly payment does not cover your accruing interest, then that monthly interest would be waived and not added to your balance.

– For example, if your monthly payment is $100 and you owe $150 a month in interest, then the government will waive the remaining $50.

Forgiveness after 30 years (previously 20–25 years)

Current borrowers will also have access to RAP.

SAVE, PAYE, and ICR Are Going Away

The new law phases out three existing income-driven IDR plans:

SAVE (from the Biden administration) will be eliminated

PAYE and ICR will also be discontinued

Only IBR (Income-Based Repayment) will remain:

For existing borrowers (loans before July 1, 2026)

Will not be available for new borrowers (loans on or after July 1, 2026)

Why is IBR sticking around?

– IBR was enacted by Congress—not created by the Department of Education—so it remains in place. Terms vary: Loans from before July 2014: payments capped at 15% of discretionary income (25-year loan forgiveness). Loans from after July 2014: capped at 10% (20-year loan forgiveness)

Who should stay on IBR?

– Lower or middle income borrowers will likely see lower payments under RAP. However, borrowers with older loans and long repayment histories may benefit from staying on IBR to reach forgiveness sooner (at 20 or 25 years).

If you’re currently on SAVE, be aware:

Interest will begin accruing again after August 1, 2025

Monthly payments may increase, especially if you previously had $0 payments

Borrowers on SAVE, PAYE, or ICR must choose between RAP or IBR by July 1, 2028—or risk being automatically placed into the Standard Plan, which could result in much higher monthly payments.

Limited Forbearance & No More Deferments

Starting July 1, 2027, deferments for economic hardship and unemployment will be eliminated for new loans. Instead:

Borrowers can use up to 9 months of forbearance within any 24-month period

Interest will continue to accrue during forbearance periods

Equity Concerns & Who’s Most Affected

The bill aims to make the loan system more financially sustainable—but it could also create new challenges for some groups:

Graduate & professional students may hit borrowing caps and turn to private loans

Low-income families, especially those relying on Parent PLUS loans, may struggle under new caps

Current SAVE borrowers could see payments jump by hundreds of dollars per month

Early estimates suggest the average borrower in SAVE may pay $3,000–$4,000 more over the life of their loan under RAP.

What Borrowers Should Do Right Now

Here’s how you can prepare before the new rules take effect:

Review your current repayment plan and understand how it will change

Estimate your future monthly payments under RAP or IBR using a loan simulator

Plan ahead for grad school funding—especially if you’re applying in the next two years

Speak with a wealth advisor or financial planner

Track important deadlines: New loan limits take effect July 1, 2026 and REPAYE/PAYE/ICR must be switched by July 1, 2028

Final Thoughts

The One Big Beautiful Bill Act marks a major shift in the student loan landscape. Whether it simplifies your path or makes repayment more complex depends on your unique situation. The best thing you can do right now is stay informed and take action early.

Student loans are changing—but you’re not alone. With the right knowledge and support, you can navigate these changes and make smart decisions for your financial future.