The Secret Math of Your ESPP + H2O: Why a 15% Discount is Worth Way More Than 15% (And How This Relates to Event Bottled Water)

If your company offers an Employee Stock Purchase Plan (ESPP), you’ve probably heard it described as a fantastic perk or "free money." If your plan includes a 15% discount and a lookback period, it isn’t just a good perk — it's a great one, and mathematically one of the highest-yielding, lowest-risk investment vehicles available to you.

Most people look at a 15% discount and assume they are getting a 15% return on their money, but that's not considering the full picture.

When you factor in how the discount actually works, how a lookback provision amplifies gains, and most importantly the actual time your cash is tied up, a core component of the time value of money, them your true annualized rate of return can skyrocket into the triple digits. Let's pull back the curtain on the math.

Part 1: How an ESPP Works (The Mechanics)

An ESPP allows you to buy company stock through automatic, post-tax payroll deductions. The process moves through a few key stages:

Offering Period: A designated timeframe (usually 6 months) where money is gradually withheld from each of your paychecks.

The Lookback Provision: This feature dictates that your purchase price is calculated using the stock price on either the first day of the offering period (the Grant Date) or the last day (the Purchase Date), whichever is lower. This is especially beneficial when your company stock price has increased from the beginning of the offering period, since you're receiving a 15% discount on a price that's even lower than present market value.

The Purchase Date: At the very end of the 6 months, the company pools all your accumulated cash and buys shares on your behalf at the discounted lookback price.

Part 2: The Baseline Return (It's 17.65%, Not 15%)

Let’s establish the baseline return assuming the stock price stays perfectly flat.

Imagine your company's stock is worth $100 at both the start and the end of a 6-month period. Because of your 15% discount, you get to buy that $100 stock for $85.

If you sell that share immediately on the purchase date, your profit is $15. To find your Return on Investment (ROI), divide your profit by what you actually paid:

i.e. ROI = $15 / $85 = ~17.65%

By merely executing the discount, you have secured a 17.65% total return on your outlay, even if the stock didn’t move a single penny.

The ability to quickly, predictably, and consistently sell something at a guaranteed discount in an existing marketplace is an example of arbitrage, in a similar way that someone selling bottled water outside of a sporting / music event (Austin FC at Q2 or Miguel at Moody Amphitheater, anyone??) is capitalizing on that same principle -- buy at a lower cost and resell at a higher cost to a market willing to accept that. The primary difference in the ESPP example is that the discount itself is locking in your return when you go to a public market and sell at the prevailing price the market was already willing to purchase at, not a convenience-based markup like the bottled water based on a captive audience.

Part 3: Factor in Time (The True Annualized Return)

An absolute return of 17.65% over six months sounds great, but to more accurately compare it to other investments in a risk-adjusted manner (like the stock market or a high-yield savings account), we must look at the Annualized Return based on how long your money was actually tied up -- it's holding period -- given that liquidity is a primary component of risk.

When you participate in a 6-month ESPP, your money isn't tied up for the full 6 months.

Your first paycheck contribution is held for the full 6 months.

Your middle paycheck contribution is held for 3 months.

Your last paycheck contribution is held for only a few days before the purchase.

On average, your money is only tied up for 3 months (0.25 years).

To calculate the Internal Rate of Return (IRR) or the true annualized return of these staggered cash flows, we look at earning a 17.65% return on money that was held, on average, for a quarter of a year:

i.e. Annualized Return = (1 + 0.1765)^4 - 1 = ~91.6%

The Reality: Assuming a flat stock price and an immediate sale on the purchase date, your money is working for you at an effective annualized rate of approximately 91.6%.

Part 4: The Lookback Supercharger

Everything we calculated above assumes the stock price stagnated. What happens if the stock price moves? Thanks to the lookback provision, you've been given even more upside.

Scenario A: The Stock Goes Down

If the stock starts at $100 and drops to $80, the lookback triggers. Your 15% discount is applied to the lower price ($80).

Your purchase price becomes $68 ($80 less 15%).

You sell immediately at market value ($80).

Your ROI is still ($80 - $68) / $68 = 17.65%. The lookback completely protects your downside.

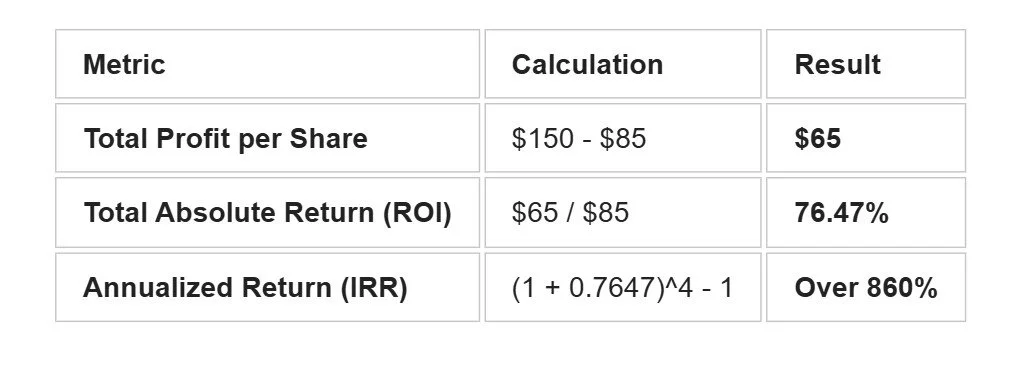

Scenario B: The Stock Goes Up (The Jackpot)

If the stock starts at $100 and increases to $150 by the end of the six months, the lookback locks in the lower original price ($100).

Your purchase price is calculated from the start date: $85 ($100 less 15%).

On the purchase date, you buy the stock for $85 and can immediately sell it for the current $150 market price.

This math makes the example even more compelling:

Because your purchase price was anchored to the past, you capture 100% of the six-month stock growth on top of your baseline discount. When annualized against the brief period your cash was tied up, the performance numbers become astronomical. This is where the time value of money really shows its strength -- being able to lock in a return that's guaranteed by nature of discount, without having to lock money up for an extended period of illiquidity.

"So Then, What's the Catch?? And Why Did I Just Pay $5 For Room-Temp Aquafina?? My Legs Hurt."

Note that one of the caveats to what may sound like an endlessly beneficial strategy is simply that IRS imposes a statutory limit on the amount that can be purchased per taxpayer, to ensure that these tax-advantaged plans stay in compliance to be able to continue offering that benefit to employees, much in the same way that ERISA governs 401(k) and other defined contribution plans.

The mechanics of this rule can sometimes catch people by surprise.

1. It is Based on Fair Market Value, Not Your Cash Contribution

The $25,000 limit is calculated using the Fair Market Value (FMV) of the stock on the first day of the offering period (the Grant Date), completely ignoring your 15% discount.

Because the limit is based on un-discounted stock value rather than the cash you spend, you will actually hit the IRS ceiling before you physically contribute $25,000.

The Math with a 15% Discount:

Suppose the stock price on Day 1 of the offering period is $100.

The IRS caps your annual purchases at 250 shares ($25,000 / $100).

With your 15% discount, you pay $85 per share.

Your maximum actual out-of-pocket cash contribution is limited to $21,250 (250 shares x $85).

If you try to contribute more than that, your company will simply refund the excess cash to you after the purchase date.

2. When Stock Prices Drop, the Limit Hits Sooner

The "Grant Date FMV" rule means the IRS limit effectively locks in a maximum number of shares you can buy on Day 1. If the stock price plummets during the 6-month period, you will hit the IRS ceiling with even less cash.

The Math if Stock Drops:

The stock starts at $100 (granting you the right to buy up to 250 shares).

The stock price drops to $50 on the purchase date.

Your lookback discount applies to the lower price, meaning you buy shares at $42.50 ($50 less 15%).

Because you are still legally capped at 250 shares for the year, your maximum cash contribution drops to just $10,625 (250 shares x $42.50). Any extra money you contributed will be refunded to you.

3. The Multi-Year "Stacking" Rollover Exception

The $25,000 limit applies to each calendar year that the offering period is active. If your company offers long, multi-year offering periods (like a 12-month or 24-month period with multiple 6-month purchase intervals), you can sometimes "stack" unused limits.

For example, if an offering period starts in late 2026 and ends in 2027, and you didn't buy any stock in 2026, you might be allowed to roll over that unused 2026 cap room, allowing you to buy more than $25,000 worth of stock in 2027.

4. Company Limits Are Often Stricter

While the IRS sets the legal ceiling at $25,000 of stock value, individual employers almost always implement their own, stricter guardrails to ensure the plan remains compliant. Common employer limits include:

Salary Percentage Caps: Restricting you to contributing a maximum of 10%, 15%, or 20% of your base salary.

Share Volume Caps: Restricting you to a maximum number of shares per purchase period (e.g., no more than 500 shares per 6 months), regardless of the stock price

The Ultimate Takeaway

An ESPP with a 15% discount and a lookback period is less of a traditional "investment" and more of a highly optimized savings vehicle.

If your financial situation allows it and your plan permits an immediate sale upon purchase, maximizing your ESPP contributions is one of the most efficient ways to build wealth. You are exposing your money to a brief, average 3-month holding period to capture a minimum annualized yield of ~91%—with an open-ended ceiling if your company's stock performs well.

Disclaimer: This article is for educational purposes only and does not constitute financial or tax advice. ESPP tax treatments (Qualifying vs. Disqualifying dispositions) vary based on how long you hold the shares after purchase. Consult a certified financial planner or tax professional regarding your personal situation. Pioneer Wealth Management Group's advisory team is designed and well-equipped to help you better understand the specifics of your company's plan, and help you make the most of your money with personalization, confidence and peace of mind.