The 5 Most Common Mistakes Google Employees Make With GSUs

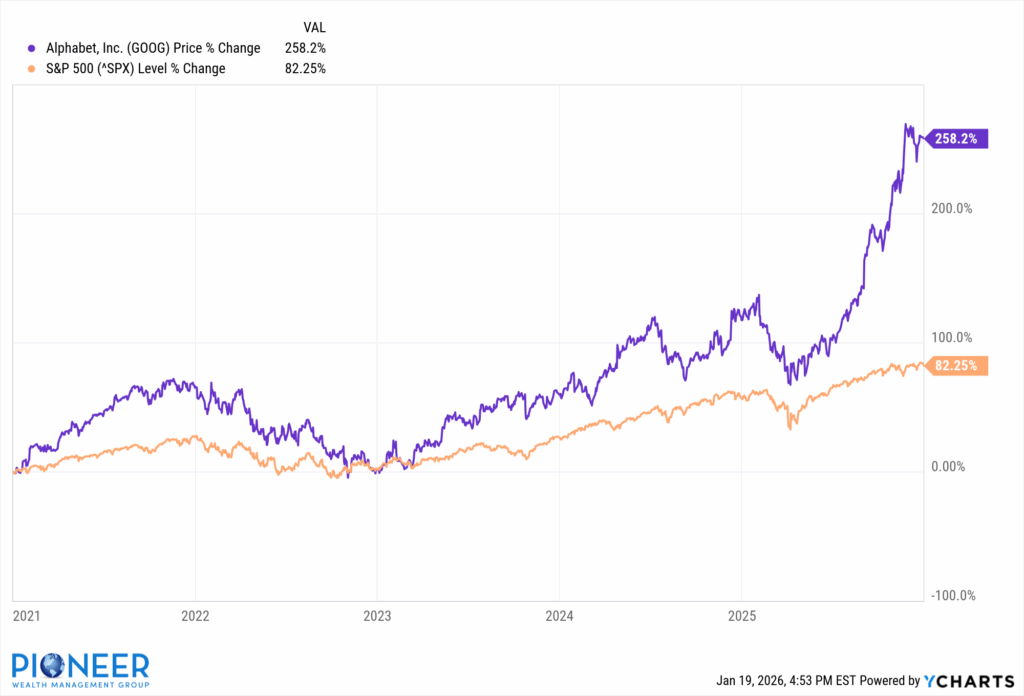

Over the five years ending December 2025, Google’s stock price significantly outperformed the S&P 500.

This level of performance naturally shapes how employees think about their stock compensation. Google is a highly innovative company, and there are many reasons to feel excited as a shareholder.

Strong stocks returns create confidence and optimism. They can also quietly increase your risk.

When a stock performs exceptionally well for an extended period, it becomes difficult to imagine a different outcome. Selling shares and diversifying can feel unnecessary (or even illogical).

The challenge is that wealth creation and risk management must coexist.

In our view, the recent performance of your GSUs presents a rare opportunity. Managed thoughtfully, your stock can accelerate financial goals and play a central role in building long-term family wealth.

These are the most common mistakes we see Google employees make with GSUs, and why adopting a clear decision framework is critical.

Mistake #1: Allowing GOOG to Become Your Largest Investment by Default

GSUs vest, shares are deposited, and life moves on. If the stock performs well, those shares grow. Then the next vest arrives, and the cycle continues. Years later, many Google employees look up and realize that GOOG now represents a surprisingly large portion of their net worth.

For Google employees, this concentration creates risk on two fronts. Your income (salary, GSUs, bonus) and your balance sheet assets (GOOG stock you own) are both heavily tied to the company’s performance.

In addition to vested shares, Google employees often overlook the exposure created by unvested GSUs (granted shares that haven’t been received yet). While these shares are not yet on the balance sheet, they represent future value that you will take ownership of in the future. This unvested exposure is not optional and cannot be diversified away.

When a company is performing well, equity compensation can feel like a powerful tailwind toward your financial goals. However, during periods of stock underperformance, company challenges, or economic decline, that same exposure can create high levels of stress and uncertainty.

Mistake #2: Assuming Taxes Are Fully Handled at Vest

When GSUs vest, taxes are automatically withheld. This can create the impression that your tax obligation has been fully covered.

In practice, RSU withholding is done at supplemental wage rates, not your marginal tax rate. For high income Google employees, these rates are often not the same. The situation leads to under withholding, especially in years when the stock price has been increasing.

The problem surfaces later, when you prepare your tax return and discover a significant balance due. Oof. In many cases, we find that ongoing quarterly estimated tax payments or W-4 withholding adjustments become necessary.

Without modeling how equity compensation fits into your full tax picture, it’s easy to owe more than you expected (along with underpayment penalties & interest).

Mistake #3: Using GSUs to Support Ongoing Lifestyle Expenses

As compensation grows, GSUs can begin to feel like a reliable income stream. Many employees sell shares regularly to fund monthly living expenses, tax payments, or major purchases.

In some cases, selling stock for liquidity needs is perfectly acceptable. In others, it becomes a subtle driver of lifestyle creep.

The key risk is building fixed expenses around a variable source of wealth. GSUs are contingent on continued employment, vesting schedules, and stock price performance. When GSUs are absorbed into spending, you run the risk of relying on them to meet your family’s needs. This creates a precarious situation if the stock price declines.

Mistake #4: Holding Stock Primarily Due to Recent Performance

After a period of exceptional returns, selling can feel unnecessary, uncomfortable (or even irresponsible). Fear of missing out (FOMO) is a very real psychological phenomenon that often drives our decision making.

The internal narrative often sounds like:

What if strong performance continues?

My coworkers are staying fully invested. Why should I act differently?

Why would I diversify if Google has been beating the market?

Recent performance becomes the default expectation, and risk controls fade into the background. We intuitively know that exceptional stock performance can’t last forever. A German proverb reminds us: “Trees don’t grow into the sky.” There are natural limits on how large a company’s valuation can become.

A few useful reframing questions:

Let’s pretend all of the GOOG shares you own today were cash (instead of stock). How much of this cash pile would you invest in GOOG right now?

If you received an unexpected bonus from Google, how much of this bonus would you invest in GOOG right now?

When viewed through this lens, many employees find that a balanced exposure approach makes sense. A portion of GSUs are retained, while the other portion is sold & diversified. Diversification in this context is not about pessimism. It is about protecting the progress you’ve already made.

Mistake #5: Failing to Evolve the Strategy as Wealth Grows

Your perception of risk will naturally evolve over time. Early in your career, the focus is often on growth and opportunity. As wealth builds, priorities tend to shift toward preservation, protection, and stewardship. As the famed investor Warren Buffet once wrote “Concentration builds wealth, diversification preserves it.” Periodically stepping back to reassess where you fall on this spectrum can be an important exercise.

As GSUs grow, they influence nearly every aspect of financial planning. These aspects include: tax exposure, liquidity decisions, portfolio construction, estate planning & wealth transfer, risk management, and mapping your long-term goals.

Major life decisions also shape how GSUs should be used. Purchasing a home, getting married, funding education, supporting children, building a business, or transitioning into retirement can all change the role equity compensation plays in your broader plan.

A sound framework should evolve alongside your career and life changes. The goal isn’t to maximize short-term outcomes, but to preserve and compound wealth in a way that supports the life it is meant to fund.

Conclusion: Build a Framework for Turning Equity Into Enduring Wealth

Google’s recent stock performance has created a meaningful opportunity for employees. Many are in a position to convert GSUs into long-lasting financial security for their families. However, realizing that opportunity requires an intentional framework.

We’re not suggesting you sell all (or even most) of your GOOG shares. We’re suggesting you make a deliberate decision about managing risk. Over the last 5 years, many Google employees have become heavily invested in the company by default (due to GSU vesting and stock performance).

A clear decision framework helps answer one of the most common questions we hear:

What percentage of my total portfolio should GOOG represent?

There is no one-size-fits all answer. Instead, a maximum exposure (i.e. ceiling) should be established within the context of your financial plan.

You may have heard this common rule of thumb: “never maintain more than 10% of your portfolio in any single company.”

While this rule is rooted in sound risk management, it ignores the nuances of equity compensation. It simply isn’t useful for many Google employees. The real objective is to manage risk responsibly based on your personal situation, financial complexity, tax impact, risk tolerance, and goals.

GSUs can be the foundation of building long-lasting wealth. If you’d like help applying these concepts and creating an intentional framework, we’d be happy to help. Please reach out to us using the Contact Us page here.