Q2 2026 Markets in Review: Breadth Returns, Semiconductors Drive Emerging Markets, and the Fed's Hawkish Pivot

Rotation Away From Mega-Cap Tech

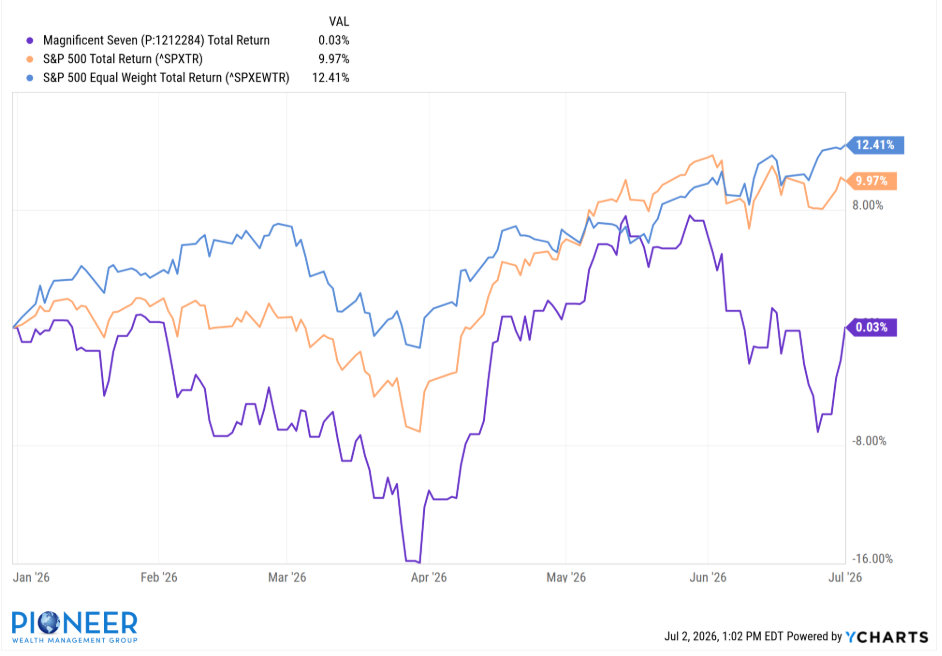

One of the more notable developments this year has been a rotation out of the Magnificent Seven and into small caps and emerging markets. It's a reversal from 2025, when emerging markets led the way, largely on the back of the semiconductor rally.

The dispersion has been significant. Several small-cap indexes are up nearly 17% year to date — roughly double the return of the broader U.S. market — while the Mag 7 as a group are essentially flat.

That flatness is the more interesting data point. The equal-weight S&P 500, which removes the outsized influence of the largest constituents, is up around 12% year to date. The gap between the cap-weighted and equal-weight index is a clear signal of expanding market breadth: performance this year has come disproportionately from the "other 493" stocks in the index rather than the handful of mega-cap names that dominated the last several years.

Data: YChart, as of July 2, 2026.

Index Construction Is Driving Real Dispersion

A useful case study in how much index methodology can matter: some emerging-markets indexes classify South Korea as a developed market and exclude it, while others — including Dimensional's — include it. That single classification difference produced roughly a 20-percentage-point performance gap between similar emerging-market strategies last year.

The reason is straightforward. South Korea has been at the center of the semiconductor boom. Samsung and SK Hynix, the country's two dominant chipmakers, both saw triple- to quadruple-digit percentage gains last year as DRAM chips became one of the tightest bottlenecks in AI infrastructure buildouts, with reports of chip capacity sold out for the next two years. Strategies that included South Korea captured that move; strategies that didn't, missed it.

A related pattern is showing up in factor tilts more broadly: value-oriented international strategies have lagged more traditional growth-tilted international index funds this year, as growth has outpaced value across most markets. Between the South Korea classification issue and the growth/value divergence, two funds that both describe themselves as "international" or "emerging markets" can produce meaningfully different results depending on construction rules and factor exposures.

Fixed Income: Lower Convexity, Same Uncertainty

Bond returns have been roughly flat to slightly negative on a total-return basis this year as rates have ticked higher. The more relevant point for the current environment is that bond price sensitivity to rate moves is considerably lower than it was a few years ago. When rates sat near zero during the pandemic era, small rate increases produced outsized price declines due to convexity effects near the zero bound. With rates now closer to long-term historical averages, a comparable move in rates is likely to have a materially smaller impact on bond prices.

It's also worth noting that the intermediate-term corporate bond market is less diversified than it might appear — issuance in that maturity range is concentrated among a fairly narrow set of issuers, largely banks. That concentration is a relevant consideration for anyone evaluating bond fund composition, separate from the rate outlook itself.

Data: YCharts, as of July 2, 2026

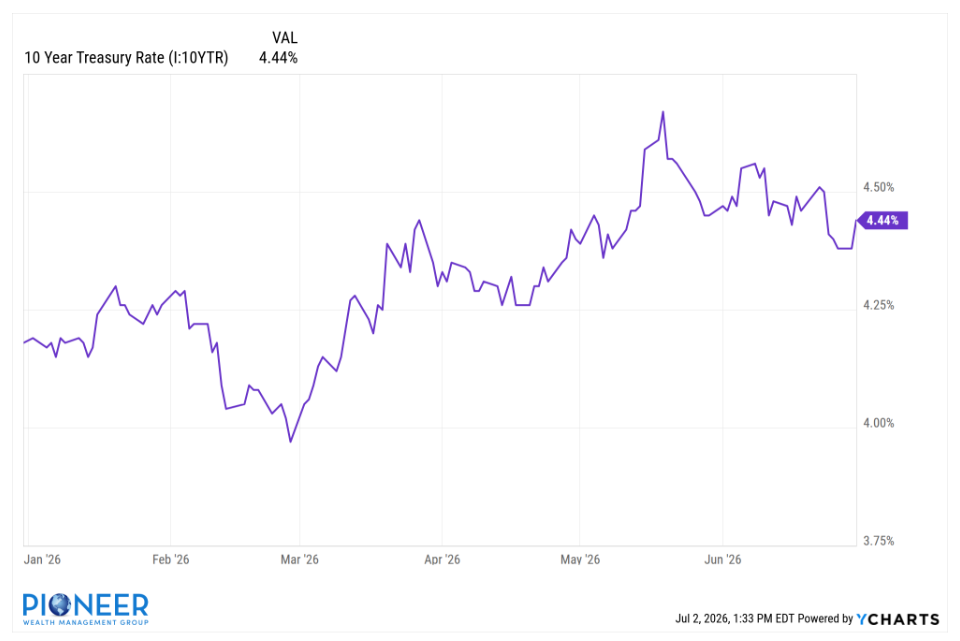

The Fed's Shift From Cuts to Hikes

Perhaps the most notable shift this year is in rate expectations themselves. Markets have moved from pricing in rate cuts to now assigning real odds to rate hikes — recent futures pricing implied roughly a 42% probability of one hike and a 28% probability of two hikes by year-end, alongside a notably more hawkish tone from the Fed under its new chair.

That said, the picture remains far from settled. A recent softer-than-expected labor report injected fresh uncertainty into the rate-hike narrative, and prediction-market odds on Fed policy have continued to swing as new data arrives. Valuations, meanwhile, remain stretched relative to historical norms — a combination worth watching given how much a hawkish surprise could weigh on already-elevated multiples.

Summary

The dominant themes this year are a broadening of market performance beyond mega-cap tech, a demonstration of how much index construction and factor tilts can affect returns even within the same asset class, and a genuine pivot in Fed rate expectations from cuts toward possible hikes. Bond markets appear better positioned to absorb further rate increases than they were several years ago, given lower convexity at current rate levels, though the path of Fed policy remains highly data-dependent and uncertain.

A broadly-diversified portfolio with stock and bond holdings across sectors and geographies tends to be the most reliable investment approach in a variety of market conditions. Speak with your financial advisor to ensure that your portfolio is aligned with your unique financial goals and wishes.

This commentary reflects general market observations as of the date discussed and should not be considered investment advice or a recommendation regarding any specific security, fund, or strategy. Past performance is not indicative of future results.