Monarch vs. YNAB: Which One is Right for You?

Most of us know that being aware of where your money goes and having a budget are important factors in one’s financial health. Just in case you don’t, here’s why it matters. Having a solid idea of your expenses informs much of the rest of your financial life - from determining how large of an emergency fund you should have, to how much you can save, to how much money you’ll ultimately need in retirement.

So yes, expense tracking and budgeting are crucial tools in your financial toolkit, but which software is right for you? This article compares two of our favorite apps at Pioneer Wealth, Monarch and YNAB (You Need A Budget), so that you can decide for yourself.

Similarities

To start, there are many similarities between the two platforms. Both allow you to customize categories and subcategories so they fit your unique financial situation. Each provides a clear visual of your budget, showing the budget, how much you’ve spent so far, and what remains for each category. You’re also able to invite collaborators so you can budget with others in your household - though Monarch allows unlimited collaborators, while YNAB allows up to five before adding a charge. Both platforms allow you to move funds between categories, meaning if you overspend in one area, you can reallocate money from another category with excess cash, helping you stay on track overall.

There are also features that differ slightly in execution but remain similar in spirit. One example is the handling of irregular expenses. Each platform helps you plan for larger, less frequent costs by breaking them into smaller monthly amounts. For instance, an annual $1,200 insurance premium can be incorporated into your budget by setting aside $100 per month, preventing your cash flow from being disrupted in the month the expense is paid.

Monarch

Now let’s discuss the differences between the platforms. Monarch’s budgeting approach is more in line with traditional budgeting software. It allows you to set spending limits for different categories based on your expected monthly income, with a focus on forecasting. Monarch organizes your budget into three primary groups:

Fixed expenses, which are relatively consistent month to month (such as mortgage, insurance, and utilities)

Flex expenses, which vary more (like dining out, entertainment, shopping, and pets) and allow you to set a combined budget across subcategories

Irregular expenses, which were mentioned earlier. In Monarch, these are planned for over time and work with its rollover feature so unused funds can carry forward until the expense is paid.

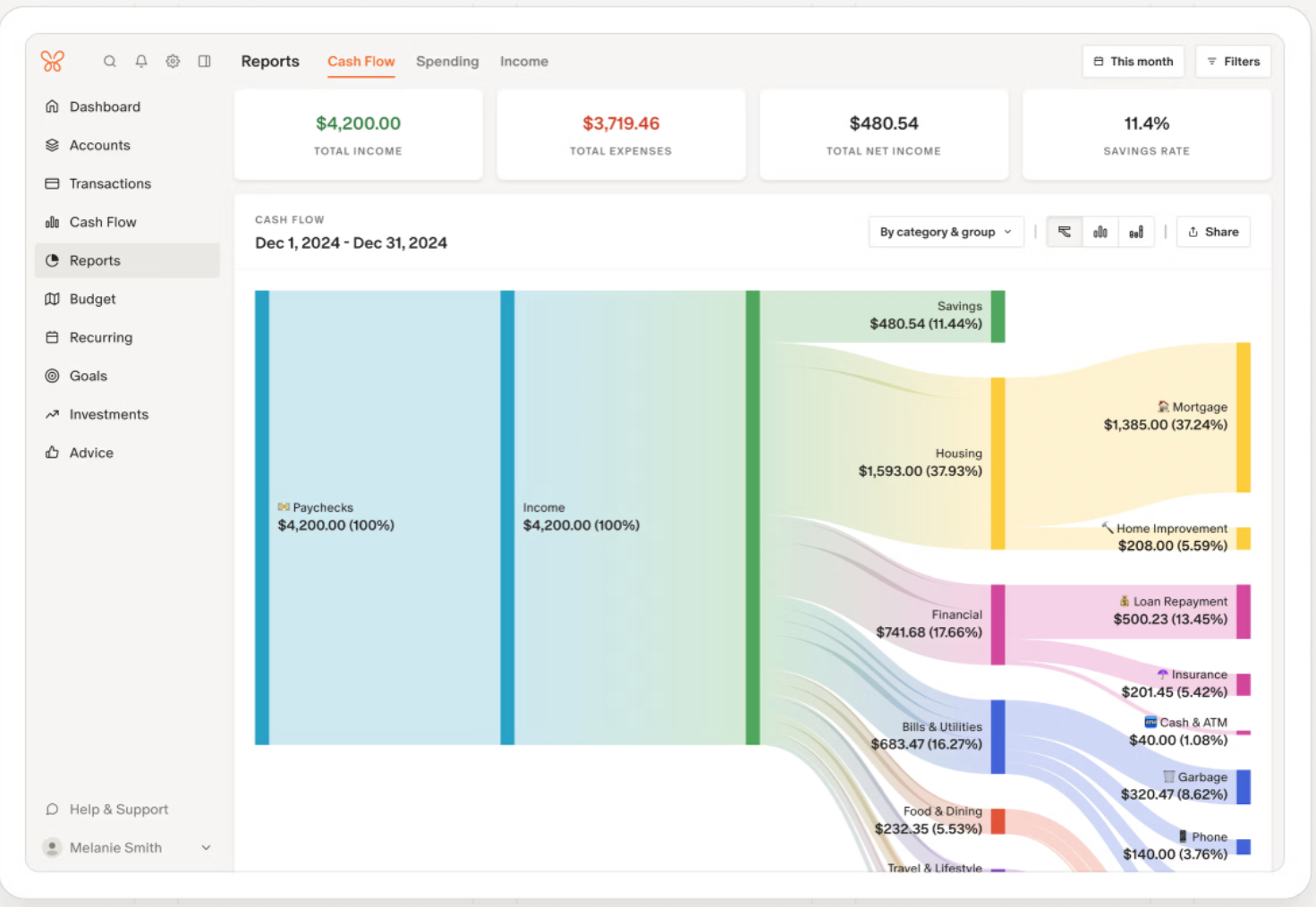

Another area where Monarch stands out is reporting. It offers more robust and visually appealing reporting than YNAB, including the fan favorite Sankey diagram that helps you clearly visualize your cash flow. Monarch also features a customizable dashboard where you can track your credit score and monitor the performance of your investment accounts, which are capabilities not currently offered by YNAB.

Monarch’s Sankey diagram.

YNAB

YNAB, on the other hand, takes a fundamentally different approach. It uses zero-based budgeting, meaning every dollar you have is assigned a job. Rather than forecasting based on expected income, YNAB focuses only on the cash you currently have on hand. Each time you receive income, you allocate the funds to your categories. YNAB also features monthly rollovers, which changes the funds in your categories based on the previous month. This approach is based on the envelope system, which can be confusing at first, but is also a powerful tool once mastered as it requires you to be more aware of your spending and budgeting.

YNAB also places an emphasis on education, with features like its debt payoff tools showing how making extra payments affects both the timeline of your debt and the total interest paid, along with several other tools designed to help users better understand and improve their financial habits over time. This ties into the fourth rule of YNAB, which is really more of a goal; Age Your Money. This means breaking the paycheck-to-paycheck cycle, with the benchmark being the ability to pay expenses using money earned at least 30 days ago.

Ultimately, choosing between Monarch and YNAB comes down to how involved you want to be in your budgeting process. YNAB requires more attention and hands-on engagement, resulting in a steeper learning curve. It encourages greater awareness of your spending which can be good for users who want to change the way they think about money. Monarch, by contrast, provides a higher-level overview of your finances while requiring less day-to-day involvement. Its forecasting approach, reports, and more automated budgeting make it a good fit for users who want clarity and insight without as much hands-on management. Both are effective tools for creating and managing a budget, so how you choose to do it is up to you!