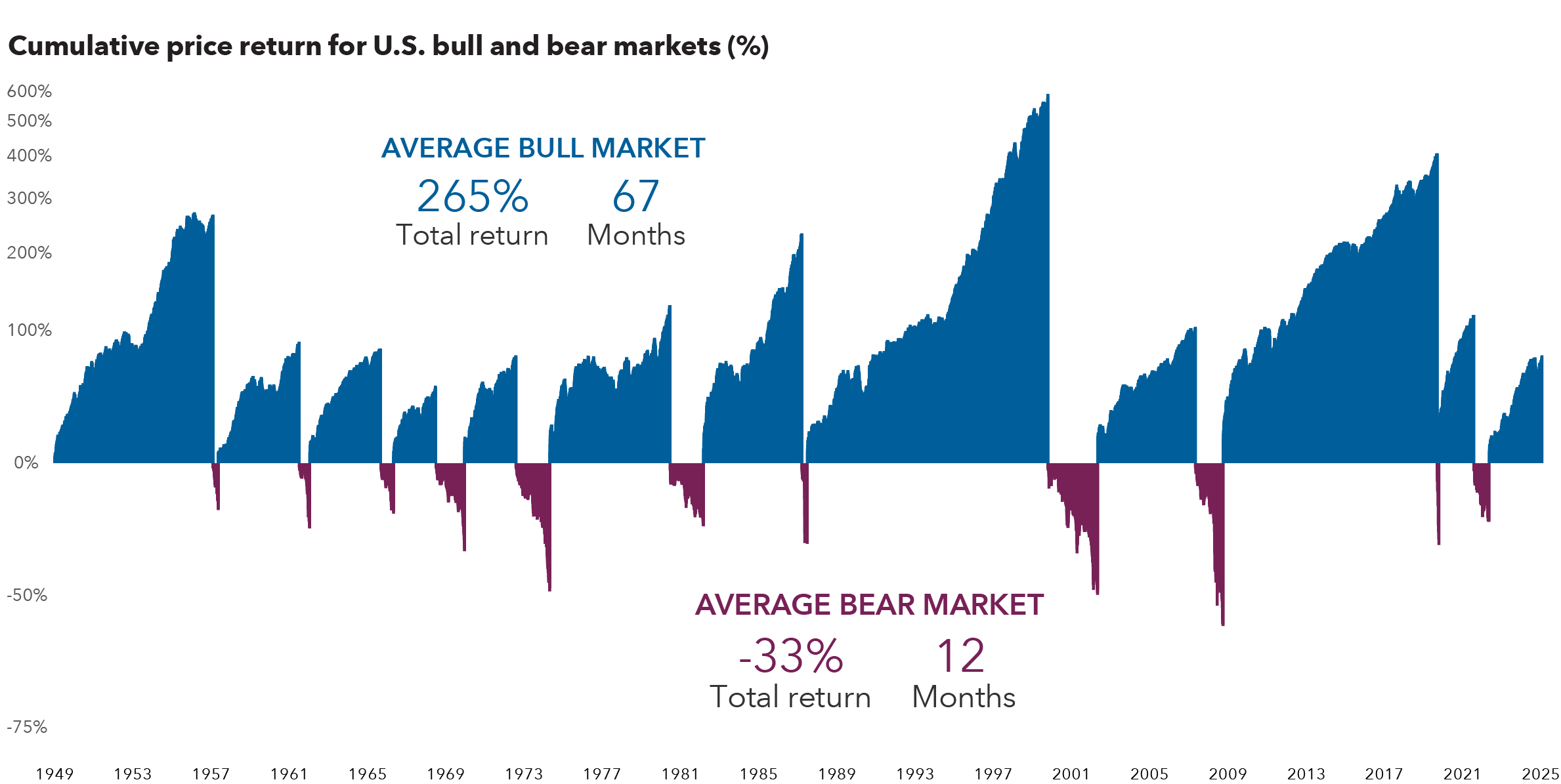

Markets don’t feel symmetrical, but more often than not they behave that way.

Many data-driven equity analysts including make the observation that markets tend to be symmetrical on the way down and on the way up. This runs counter to how most investors experience volatility. When markets fall, it feels chaotic, prolonged, and uncertain. When they rise, it often feels fragile, undeserved, or temporary. That emotional asymmetry leads investors to predict drawn-out recoveries, U-shapes, L-shapes, K-shapes, etc. History repeatedly delivers something much simpler: a V.

This disconnect starts with human nature. Investors anchor their expectations to what feels reasonable in the moment. During downturns, the news flow is overwhelmingly negative. Earnings revisions, layoffs, geopolitical risks, tightening financial conditions are terrifying in the moment. It’s easy to extrapolate that environment forward and assume recovery will be slow and uneven. A sharp rebound feels unlikely because it doesn’t match the prevailing narrative. Markets don’t move based on comfort or consensus. They move based on positioning, expectations, and the rate of change.

By the time conditions feel the worst, markets have often already priced in a significant amount of bad news. Selling pressure becomes exhausted. Cash builds on the sidelines. Expectations get reset lower. It doesn’t take perfect news to spark a recovery. Just “less bad” than feared is often what’s necessary. When that shift happens, the move higher can be just as fast and forceful as the decline. That’s where the symmetry comes in.

The same mechanics that accelerate declines (panic, forced selling, de-risking) can reverse on the way up. Investors who sold late rush back in. Underinvested portfolios chase performance. Short positions get covered. Liquidity improves. The result is a rapid, often uncomfortable rally that mirrors the speed of the drop.

We’ve seen this pattern play out repeatedly. The 2020 pandemic crash erased years of gains in a matter of weeks only to recover them just as quickly. The 2018 Q4 selloff reversed sharply once policy expectations shifted. Even earlier cycles, despite different catalysts, show a similar rhythm: fast down, fast up. Yet each time, the dominant narrative during the downturn insists that “this time is different.”

Investors reach for new shapes (U, W, K) not because they’re supported by data, but because they feel more intuitive. A slow healing process seems more logical than a sudden recovery. It aligns with how we process bad experiences in real life, where damage takes time to repair. Markets aren’t a reflection of lived experience. They’re a forward-looking mechanism constantly repricing expectations.

None of this means every recovery is perfectly symmetrical or that volatility disappears. There are always deviations, false starts, and uneven leadership beneath the surface. At a high level, the market’s tendency toward V-shaped behavior is more persistent than most investors are willing to admit.

The practical implication is uncomfortable but important: waiting for clarity often means missing the recovery. By the time the outlook feels stable again, markets have typically already moved. The steepest part of the rebound happens when uncertainty is still high and confidence is still low. That’s precisely when many investors remain on the sidelines, expecting a more “reasonable” entry point that never comes.

Understanding this doesn’t eliminate risk, but it reframes how to think about it. Instead of trying to predict the exact shape of the next cycle, it’s more useful to recognize the market’s bias toward speed and reflexivity. Downturns can be sharp, but recoveries can be just as swift. Positioning for that reality rather than for what feels comfortable can make the difference between participating in the recovery and watching it happen from a distance.

Markets may not feel symmetrical, but history suggests they often are. As always, speak with your wealth advisors and other financial professionals to see how this information affects your personal situation.

(C) Capital Group 2025