Google L6+? Now what?

How to Think About GSUs and the Mega Backdoor Roth—Before Small Mistakes Get Expensive

Being hired into an L6+ role at Google is a different financial experience than earlier career stages. At this level, base salary matters—but equity and tax strategy are what ultimately drive long-term outcomes.

Two areas dominate the conversation for senior Googlers:

GSUs (Google Stock Units)

The Mega Backdoor Roth

Handled well, they can materially accelerate wealth. Handled casually, they can quietly create tax drag, concentration risk, and missed opportunities. This article focuses only on those two levers—and how to think about them at a senior level.

Part 1: GSUs — Your Largest Asset, Whether You Treat Them Like It or Not

For most L6+ Googlers, GSUs quickly become:

The largest source of annual income

The largest single asset on the balance sheet

The biggest driver of tax exposure

Yet many people still treat them as “bonus stock” rather than what they really are: deferred cash compensation paid in company shares.

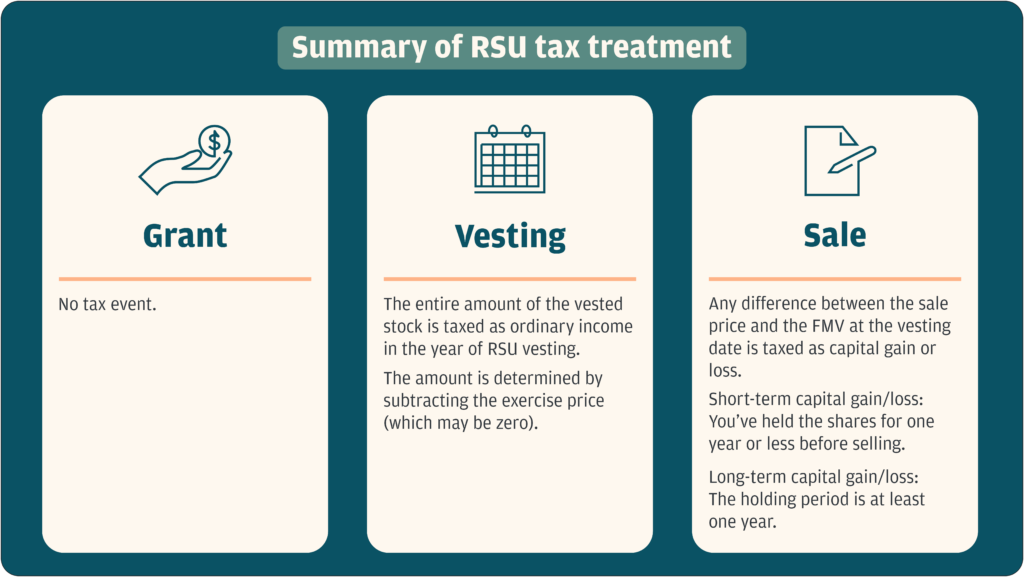

How GSUs Actually Work (At the Level That Matters)

When GSUs vest:

They are taxed as ordinary income, just like salary

Google withholds shares to cover taxes

The remaining shares land in your brokerage account

At that moment, two things happen simultaneously:

You’ve already been taxed

You now own a concentrated stock position

From a planning perspective, the vest date is the decision point—not the grant date.

© JP Morgan Workplace Solutions

The Biggest GSU Mistake L6+ Employees Make

The most common (and costly) mistake is inaction by default:

Letting vested shares accumulate

Assuming withholding was “close enough”

Never defining a sell vs. hold framework

Over time, this often leads to:

40–70%+ of net worth tied to one company

Large, unintentional market risk

Tax inefficiency disguised as loyalty or optimism

This isn’t about being bearish on Google. It’s about recognizing that career risk and equity risk are already correlated.

A Better Way to Think About GSUs

A more useful question than “Should I sell?” is: “If I were paid this income in cash, would I choose to invest it all back into Google stock?”

For most L6+ employees, the honest answer is no—at least not at that scale. That realization reframes GSUs from an emotional decision into a portfolio one.

Smart GSU Strategy at Senior Levels

Well-designed GSU strategies usually include:

A rules-based sell framework rather than ad hoc decisions

Gradual diversification over time

Intentional use of proceeds, not idle cash

Integration with tax and retirement planning

The goal is not to time Google stock. The goal is to control concentration while preserving upside exposure aligned with your broader plan.

Part 2: The Mega Backdoor Roth — One of the Few Places You Can Still Win the Tax Game

At L6+ compensation levels, most traditional tax shelters phase out. That’s what makes the Mega Backdoor Roth so powerful—and so often misunderstood.

What the Mega Backdoor Roth Actually Is

In plain terms, it allows you to:

Contribute after-tax dollars to your 401(k)

Convert those dollars into a Roth account

Achieve long-term tax-free growth, even at high income levels

For senior Googlers, this can mean tens of thousands of dollars per year moving into a tax-free bucket—legally and systematically.

Why This Matters More at L6+

At senior compensation levels:

Marginal tax rates are high

Future tax uncertainty is real

Traditional pre-tax savings alone often create future tax concentration

The Mega Backdoor Roth helps balance this by building tax diversification across:

Pre-tax assets (traditional 401(k))

Taxable assets (brokerage accounts, GSUs)

Tax-free assets (Roth accounts)

That balance is what creates flexibility later in life.

Common Mega Backdoor Roth Pitfalls

Even highly compensated Googlers often:

Don’t realize they’re eligible

Miss the timing window

Leave funds sitting in after-tax status too long

Fail to coordinate conversions properly

The opportunity isn’t just contributing—it’s executing correctly and consistently.

Why GSUs and the Mega Backdoor Roth Belong in the Same Conversation

This is where senior-level planning becomes powerful.

GSUs create:

High taxable income

Cash flow from share sales

Concentration risk

The Mega Backdoor Roth provides:

A tax-free destination for excess cash

A way to convert high income into long-term flexibility

A counterweight to taxable equity compensation

When coordinated intentionally, GSUs can fund Roth strategies that materially improve after-tax outcomes over time.

A Simple L6+ Framework (Not a Checklist)

Rather than optimizing each decision in isolation, strong plans answer:

How much Google exposure do I want over time?

What is my long-term tax mix—not just this year’s bill?

Where should excess cash from GSUs go on purpose?

The answers will evolve, but the framework prevents drift.

Final Thought: Senior Compensation Requires Senior-Level Intentionality

At L6+, the risk isn’t that you’re underpaid. It’s that complexity quietly works against you if left unmanaged. GSUs and the Mega Backdoor Roth are two of the most powerful tools available to senior Googlers—but only when they’re coordinated thoughtfully. The goal isn’t to optimize everything immediately. It’s to ensure that the biggest levers in your financial life are pulling in the right direction.